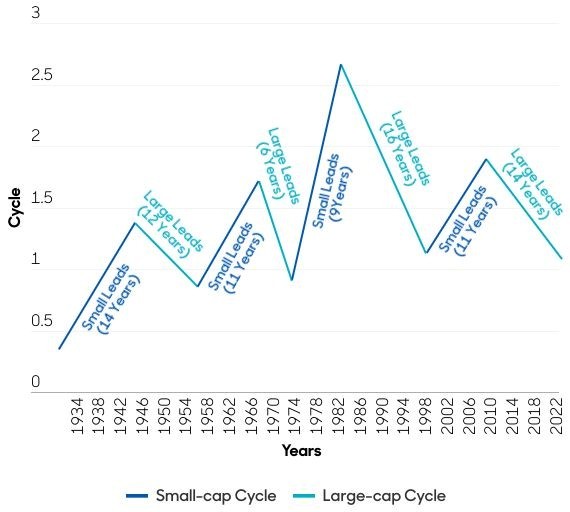

While academics debate the validity of the “small cap effect” (i.e. small caps are less efficient/ riskier, thus requiring a higher level of return to attract investors), the practical answer is simple: if the small cap effect existed, it has now seemingly vanished – at least in the U.S. The Russell 1000 outperformed the Russell 2000 counterpart by more than 1000 and 800 basis points for the one- and three-year periods respectively ending March 31, 2025. The discrepancy was exacerbated by the election, as the small-cap benchmark fell 22% (technically bear market territory) from its postelection high on Nov. 25, 2024 through April 4, 2025.

But that weakness may be transient. The U.S. small-cap index has historically rebounded with average gains of 6.8% over the three months after entering a bear market, and nearly 12% over the following six months, according to Dow Jones Market Data. So don’t write off U.S. small caps just yet … history, valuation and macro conditions suggest a comeback in 2025.

Why such a big dislocation between large and small caps?

For value investors like us, small caps offer the perfect trifecta: 1) diversification and cyclical industry exposure in marked contrast to the tech-heavy large cap concentration, 2) attractive valuations, looking heavily discounted compared to larger peers on both an absolute and relative basis and 3) a fertile hunting ground in an inefficient investment universe that may be bound for a resurgence in 2025.

IMPORTANT INFORMATION:

This material is intended for information purposes only, and does not constitute: (i) financial, economic, legal, investment, accounting, or tax advice, (ii) a recommendation or an offer or solicitation to purchase or sell any securities or (iii) a recommendation for any investment product or strategy mentioned herein. Polaris Capital Management (“Polaris”) has no obligation to provide updated information on the securities/instruments mentioned herein.

The opinions expressed are those of Jason Crawshaw of Polaris Capital as of the date shown above, and are subject to change without notice. Information, particularly facts and figures, are dated and in many cases outdated; Polaris does not undertake any obligation to update such information. This information is not intended to be complete or exhaustive and no representations or warranties, either express or implied, are made regarding the accuracy or completeness of the information contained herein. Reliance upon information in this material is at the sole discretion of the reader.

Any performance information provided reflects past performance and is as of the date shown in the commentary, which may not be indicative of future results. Market conditions, macroeconomic factors, and portfolio composition may change over time and may not be reflected herein. This material may contain estimates and forward-looking statements, which may include forecasts and do not represent a guarantee of future performance.

Investing involves risks. Mid- and small-cap stocks tend to be more volatile than large-company stocks. Diversification does not guarantee a profit or protect against loss. Before investing, you should carefully consider a portfolio’s investment objectives, risks, charges and expenses. Investors should make investment decisions based on their unique investment objectives and financial situation.

The indices are unmanaged. An investor cannot invest directly in an index. They are shown for illustrative purposes only and do not represent the performance of any specific investment. The indices are not subject to expenses or fees and are often comprised of securities and other investment instruments the liquidity of which is not restricted. A particular investment product may consist of securities significantly different than those in any index referred to herein. Comparing an investment to a particular index may be of limited use.

The distribution of this publication may be restricted by law or regulation in different jurisdictions and persons into whose possession this publication comes should inform themselves about, and observe, such restrictions.

Polaris Capital is an investment adviser registered with the Securities and Exchange Commission. For more information about Polaris, please contact us at (617) 951-1365 or email Client Service.

Polaris Capital Management LLC is an investment advisor registered with the U.S. Securities and Exchange Commission (SEC). Polaris' website provides general information regarding our business along with access to additional investment related information. Material presented is meant for informational purposes only. To the extent that you utilize any financial calculators or links in our website, you acknowledge and understand that the information provided to you should not be construed as personal investment advice from Polaris or any of its investment professionals. For additional information regarding our services, or to receive a hard copy of our firm's disclosure documents (Form ADV Part I and Form ADV Part II), contact client service. You may also obtain these disclosure documents online from the SEC Investment Adviser Public Disclosure (Firm CRD# 106278). ©2013-2025 Polaris Capital Management, LLC. All rights reserved.

This website uses necessary cookies to make our site work. A handful of non-essential cookies seek to enhance the browsing experience, analyze website traffic and improve site usage and functionality via analytics. By clicking “Accept“, you consent to accept these non-essential cookies; however, you can opt-out by clicking "Deny". See our cookie policy here.

IMPORTANT INFO: RETIREMENT CALCULATOR

The retirement calculator is a model or tool intended for informational and educational purposes only, and does not constitute professional, financial or investment advice. This model may be helpful in formulating your future plans, but does not constitute a complete financial plan. We strongly recommend that you seek the advice of a financial services professional who has a fiduciary relationship with you before making any type of investment or significant financial decision. We, at Polaris Capital, do not serve in this role for you. We also encourage you to review your investment strategy periodically as your financial circumstances change.

This model is provided as a rough approximation of future financial performance that you may encounter in reaching your retirement goals. The results presented by this model are hypothetical and may not reflect the actual growth of your own investments. Polaris strives to keep its information and tools accurate and up-to-date.

The information presented is based on objective analysis, but may not be the same that you find at a particular financial institution, service provider or specific product’s site. Polaris Capital and its employees are not responsible for the consequences of any decisions or actions taken in reliance upon or as a result of the information provided by this tool. Polaris is not responsible for any human or mechanical errors or omissions. All content, calculations, estimates, and forecasts are presented without express or implied warranties, including, but not limited to, any implied warranties of merchantability and fitness for a particular purpose or otherwise.

Please confirm your agreement/understanding of this disclaimer.

DISCLAIMER: You are about to leave the Polaris Capital Management, LLC website and will be taken to the PCM Global Funds ICAV website. By accepting, you are consenting to being directed to the PCM Global Funds ICAV website for non-U.S. investors only.